米サンフランシスコ連銀のYellen総裁の経済見通し。2009年下半期は在庫圧縮ペースの減少が主な要因となってプラス成長に戻るという。ただ、雇用、個人消費は長期にわたって弱含み、V字型ではなくU字型の景気回復となる見込みという。商業用不動産の損失は引き続き拡大し、雇用、設備稼働率が完全な状態に戻るには数年はかかるという。

○Fed's Yellen: The Outlook for Recovery

http://www.calculatedriskblog.com/2009/09/feds-yellen-outlook-for-recovery.html

・・・I regret to say that I expect the recovery to be tepid.

・・・ things won’t feel very good for some time to come.

・・・This summer likely marked the end of the recession and the economy should expand in the second half of this year.

・・・However, payrolls are still shrinking at a rapid pace, even though the momentum of job losses has slowed in the past few months.

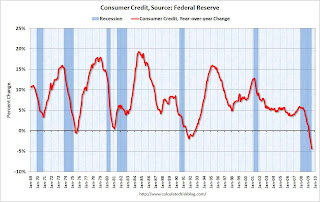

・・・ Importantly, consumer spending finally is bottoming out.

・・・A particularly hopeful sign is that inventories, which have been shrinking rapidly, now seem to be in better alignment with sales.

・・・I expect the biggest source of expansion in the second half of this year to come from a diminished pace of inventory liquidation by manufacturers, wholesalers, and retailers.

・・・the boost is usually fairly short-lived, but it can be quite important in getting things going. ...

・・・My own forecast envisions a far less robust recovery, one that would look more like the letter U than V. ...

・・・more credit losses are in store even as the economy improves and overall financial conditions ease. Certainly, households remain stressed. In the face of high and rising unemployment, delinquencies and foreclosures are showing no sign of turning around.

・・・The chances are slim for a robust rebound in consumer spending,

・・・Over the long term, consumers face daunting issues of their own.

・・・It may well be that we are witnessing the start of a new era for consumers following the traumatic financial blows they have endured.

・・・ My business contacts indicate that they will be very reluctant to hire again until they see clear evidence of a sustained recovery, and that suggests we could see another so-called jobless recovery in which employment growth lags the improvement in overall output. What’s more, wage growth has slowed sharply.

・・・Putting the whole puzzle together, the main impetus to growth in the second half of this year will be inventory investment. The boost it provides will be a big help for a while, but we will need to look to other sectors to sustain growth.

・・・Going forward, however, rising loan losses on other commercial real estate lending is likely because property values are falling, office vacancy rates are rising,

・・・The slow recovery I expect means that it could still take several years to return to full employment. The same is true for capacity utilization in manufacturing. It will take a long time before these human and capital resources are put to full use.