RSS Feed

RSS Feed by Calculated Risk on 5/08/2024 07:00:00 AM

Wednesday, May 08, 2024

MBA: Mortgage Applications Increased in Weekly Survey

From the MBA: Mortgage Applications Increase in Latest MBA Weekly Survey

Mortgage applications increased 2.6 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending May 3, 2024.

The Market Composite Index, a measure of mortgage loan application volume, increased 2.6 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 3 percent compared with the previous week. The Refinance Index increased 5 percent from the previous week and was 6 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 2 percent from one week earlier. The unadjusted Purchase Index increased 2 percent compared with the previous week and was 17 percent lower than the same week one year ago.

“Treasury rates and mortgage rates fell last week on the news of a slowing job market, with wage growth at the slowest pace since 2021, and the Federal Reserve’s announced plans to ease quantitative tightening in June and to maintain its view that another rate hike is unlikely. The conventional 30-year rate dropped 11 basis points, and the FHA rate fell 17 basis points to 6.92 percent, back below 7% for the first time in three weeks,” said Mike Fratantoni, MBA’s Senior Vice President and Chief Economist. “Mortgage applications increased for the first time in three weeks, with refinances up 5 percent. Even with the increase, which included a 29 percent jump in VA refinances, refinance application volume remains about 6 percent below last year’s already low levels.”

Added Kan, “Driven by a 5 percent gain in FHA applications, purchase activity was up 2 percent. First-time homebuyers account for roughly half of purchase loans, and the government lending programs are an important source of financing for these homebuyers. The gain in FHA activity is a sign that this segment of the market is active.”

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) decreased to 7.18 percent from 7.29 percent, with points unchanged at 0.65 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the MBA mortgage purchase index.

According to the MBA, purchase activity is down 17% year-over-year unadjusted.

Red is a four-week average (blue is weekly).

Purchase application activity is up slightly from the lows in late October 2023, and below the lowest levels during the housing bust.

The second graph shows the refinance index since 1990.

With higher mortgage rates, the refinance index declined sharply in 2022, and has mostly flat lined since then.

Tuesday, May 07, 2024

Wednesday: Mortgage Applications

by Calculated Risk on 5/07/2024 07:49:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Wednesday:

• At 7:00 AM ET, The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

Asking Rents Mostly Unchanged Year-over-year

by Calculated Risk on 5/07/2024 11:58:00 AM

Today, in the Real Estate Newsletter: Asking Rents Mostly Unchanged Year-over-year

Brief excerpt:

Tracking rents is important for understanding the dynamics of the housing market. For example, the sharp increase in rents helped me deduce that there was a surge in household formation in 2021 (See from September 2021: Household Formation Drives Housing Demand). Now that household formation has slowed, and multi-family completions have increased, rents are under pressure.There is much more in the article.

From ApartmentList.com: Apartment List National Rent Report

Rents are up 0.5% month-over-month, down 0.8% year-over-year

Rent growth follows a seasonal pattern – rent increases generally take place during the spring and summer, whereas the fall and winter usually see a modest price dip. We are currently transitioning into the busy season, with the national median rent increasing for the third straight month, following six consecutive monthly declines from August 2023 to January 2024. However, the pace of that positive rent growth slowed slightly this month, with rents up 0.5 percent month-over-month in April, after increasing by 0.6 percent in March.

AAR: Rail Carloads Down YoY in April, Intermodal Up

by Calculated Risk on 5/07/2024 11:01:00 AM

From the Association of American Railroads (AAR) Rail Time Indicators. Graphs and excerpts reprinted with permission.

Total originated U.S. carloads averaged 212,221 per week in April 2024, down 6.5% from April 2023 and the second lowest weekly average for April in our records that go back to 1988. (April 2020 was lower.) Total carloads fell year over year each of the first four months of 2024. Year-to-date total carloads through April were down 4.8% and, at 3.62 million, were the lowest for any year in our records.

The main reason is coal. ...

U.S. railroads also originated 1.02 million intermodal containers and trailers in April 2024, up 8.6% over April 2023 — intermodal’s eighth straight year-over-year gain. (Intermodal is not included in carloads.)

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph from the Rail Time Indicators report shows the six-week average of U.S. Carloads in 2022, 2023 and 2024:

Total originated U.S. carloads in April 2024 were 848,882, down 6.5% (58,751 carloads) from April 2023. The weekly average in April 2024 was 212,221 carloads per week, the second lowest for April in our records that go back to 1988. (April 2020, when the pandemic was just starting, was lower.) Year-to-date total carloads through April were 3.62 million, down 4.8% (180,839 carloads) from last year. Total carloads fell year-over-year each of the first four months of 2024.

It’s a broken record at this point, but blame coal. In April 2024, coal averaged 46,303 carloads per week, down 28.0% from April 2023 — the fourth straight double-digit percentage decline.

The second graph shows the six-week average (not monthly) of U.S. intermodal in 2022, 2023 and 2024: (using intermodal or shipping containers):

The second graph shows the six-week average (not monthly) of U.S. intermodal in 2022, 2023 and 2024: (using intermodal or shipping containers):U.S. railroads originated 1.02 million intermodal containers and trailers in April 2024, up 8.6% (80,471 units) over April 2023 — intermodal’s eighth straight gain. In April 2024, intermodal averaged 254,642 units per week. April’s average from 2015 to 2023 was 257,701, slightly higher than April 2024. Last year wasn’t a good year for intermodal — it was the lowest since 2013 — and the gains this year have essentially returned intermodal volume back to normal.

Wholesale Used Car Prices Declined in April; Down 14.0% Year-over-year

by Calculated Risk on 5/07/2024 09:06:00 AM

From Manheim Consulting today: Wholesale Used-Vehicle Prices Declined in April

Wholesale used-vehicle prices (on a mix, mileage, and seasonally adjusted basis) were down in April compared to March. The Manheim Used Vehicle Value Index (MUVVI) fell to 198.4, a decline of 14.0% from a year ago. The seasonal adjustment to the index magnified the results for the month, resulting in a 2.3% month-over-month decrease. The non-adjusted price in April decreased by 0.6% compared to March, moving the unadjusted average price down 11.9% year over year.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This index from Manheim Consulting is based on all completed sales transactions at Manheim’s U.S. auctions.

The Manheim index suggests used car prices declined in April (seasonally adjusted) and were down 14.0% year-over-year (YoY).

CoreLogic: US Home Prices Increased 5.3% Year-over-year in March

by Calculated Risk on 5/07/2024 08:00:00 AM

Notes: This CoreLogic House Price Index report is for March. The recent Case-Shiller index release was for February. The CoreLogic HPI is a three-month weighted average and is not seasonally adjusted (NSA).

From CoreLogic: Northeast Continues to Lead US for Annual Home Price Gains in March, CoreLogic Reports

• U.S. single-family home prices rose by 5.3% year over year in March, marking the 146th consecutive month of annual growth.This was a smaller YoY increase than the 5.5% reported for February, and the 5.8% YoY increase reported for January.

• Over the next 12 months, year-over-year home price gains are projected to range between 5.6% and 3.7%.

• Four of the top five states for annual appreciation in March are in the Northeast: New Jersey (12.2%), New Hampshire (10.6%), Connecticut (9.5%) and Rhode Island (9.2%).

...

U.S. year-over-year home price gains remained above 5% in March for the fifth straight month and are projected to stay in that general range for most of the next 12 months. Northeastern states continued to post the nation’s largest gains, as more Americans migrate to bedroom communities of major cities and job hubs, as well as areas where household incomes are relatively higher and can sustain the elevated cost of homeownership. In addition, the inventory gains seen in states like Florida and Texas still lag in the Northeast, a trend that continues to exacerbate supply-and-demand fundamentals and further adds to home price pressure in that region. Consequently, markets with larger additions of homes for sale are now experiencing slowing home price appreciation.

“Home prices increased again this March beyond the typical seasonal uptick, despite mortgage rates reaching this year’s high and the affordability crunch continuing to keep many prospective buyers on the sidelines,” said Dr. Selma Hepp, chief economist for CoreLogic. “Even with the long-anticipated break in for-sale inventory, the surging cost of homeownership, further fueled by rising insurance and tax expenses, is holding potential home sales back, as is evident in the slow rise in sales compared with last year. These price pressures reflect the overall supply-and-demand mismatch, as well as continued interest from households with larger budgets.”

emphasis added

Monday, May 06, 2024

Tuesday: CoreLogic Home Price Index

by Calculated Risk on 5/06/2024 07:45:00 PM

From Matthew Graham at Mortgage News Daily: Everything is a Sideshow Until May 15th

From Matthew Graham at Mortgage News Daily: Everything is a Sideshow Until May 15th

In a world where all hope for interest rate relief hinges on disinflation, CPI dominates all other calendar events. With nearly 10 days to go until the next release (May 15th) and very little on the econ calendar between now and then, it would be a surprise to see any new directional trends emerge. [30 year fixed 7.25%]Tuesday:

emphasis added

• At 8:00 AM ET, CoreLogic Home Price Index for March

Fed SLOOS Survey: Banks reported Tighter Standards, Weaker Demand for almost All Loan Types

by Calculated Risk on 5/06/2024 02:49:00 PM

From the Federal Reserve: The April 2024 Senior Loan Officer Opinion Survey on Bank Lending Practices

The April 2024 Senior Loan Officer Opinion Survey on Bank Lending Practices (SLOOS) addressed changes in the standards and terms on, and demand for, bank loans to businesses and households over the past three months, which generally correspond to the first quarter of 2024.

Regarding loans to businesses, survey respondents reported, on balance, tighter standards and weaker demand for commercial and industrial (C&I) loans to firms of all sizes over the first quarter. Meanwhile, banks reported tighter standards and weaker demand for all commercial real estate (CRE) loan categories.

Banks also responded to a set of special questions about changes in lending policies and demand for CRE loans over the past year. For all CRE loan categories, banks reported having tightened all queried lending policies, including the spread of loan rates over the cost of funds, maximum loan sizes, loan-to-value ratios, debt service coverage ratios, and interest-only payment periods.

For loans to households, banks reported that lending standards tightened across some categories of residential real estate (RRE) loans while remaining unchanged for others on balance. Meanwhile, demand weakened for all RRE loan categories. In addition, banks reported tighter standards and weaker demand for home equity lines of credit (HELOCs). Moreover, for credit card, auto, and other consumer loans, standards reportedly tightened and demand weakened.

While banks, on balance, reported having tightened lending standards further for most loan categories in the first quarter, lower net shares of banks reported tightening lending standards than in the fourth quarter of last year across most loan categories.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph on Residential Real Estate demand is from the Senior Loan Officer Survey Charts.

This graph is for demand and shows that demand has declined.

The left graphs are from 1990 to 2014. The right graphs are from 2015 to Q1 2024.

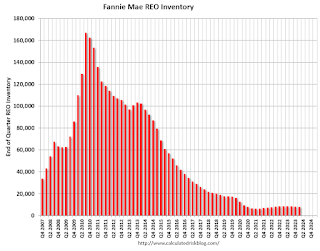

Fannie "Real Estate Owned" inventory Decreased in Q1 2024

by Calculated Risk on 5/06/2024 02:01:00 PM

Fannie reported results for Q1 2024. Here is some information on single-family Real Estate Owned (REOs).

Fannie Mae reported the number of REOs decreased to 7,791 at the end of Q1 2024, down 5% from 8,403 at the end of the previous quarter, and down 9% year-over-year from Q1 2023.

For Fannie, this is down 95% from the 166,787 peak number of REOs in Q3 2010.

Click on graph for larger image.

Click on graph for larger image.

Here is a graph of Fannie Real Estate Owned (REO).

This is well below the normal level of REOs for Fannie, and there will not be a huge wave of foreclosures.

Click on graph for larger image.

Click on graph for larger image.Here is a graph of Fannie Real Estate Owned (REO).

This is well below the normal level of REOs for Fannie, and there will not be a huge wave of foreclosures.

ICE Mortgage Monitor: Annual home price growth eased in March; "For-sale inventory has been growing sharply across Florida"

by Calculated Risk on 5/06/2024 11:01:00 AM

Today, in the Real Estate Newsletter: ICE Mortgage Monitor: Annual home price growth eased in March

Brief excerpt:

Press Release: ICE Mortgage Monitor: Historically Strong Home Price Growth Pushes U.S. Mortgage Holders’ Tappable Equity to Record $11TThere is much more in the article.Here is the year-over-year in house prices according to the ICE Home Price Index (HPI). The ICE HPI is a repeat sales index. Black Knight reports the median price change of the repeat sales. The index was up 5.6% year-over-year in March, down from 6.0% YoY in February.

• Home price growth slowed in March, driven by a tightening of both mortgage rates and home affordability, but continues to remain historically strong

• Annual home price growth eased from an upwardly revised 6.0% in February to +5.6% in March, with prices rising by a seasonally adjusted +0.42% in the month, down from a revised +0.58% in February

• On a non-adjusted basis, prices were up +1.2% in March, more than 25% above the 25-year March average of +0.96%

• March marked the third straight month of above average monthly growth, after monthly gains fell below the 25-year average in five of the final six months of 2023, dampened by elevated interest rates

• While rising interest rates suppressed purchase demand and allowed modest inventory growth this spring, prices have remained resilient so far

• That said, adjusted monthly growth continuing at or near its currently rate would result in modestly slowing annual home price growth as we move into summer